Cheapest home insurance for high-risk areas sets the stage for exploring cost-effective insurance options in regions prone to risks. Discover how homeowners can secure their properties without breaking the bank.

Delve into the factors influencing insurance rates, effective cost-saving strategies, comparisons of insurance providers, and the significance of adequate coverage in disaster-prone areas.

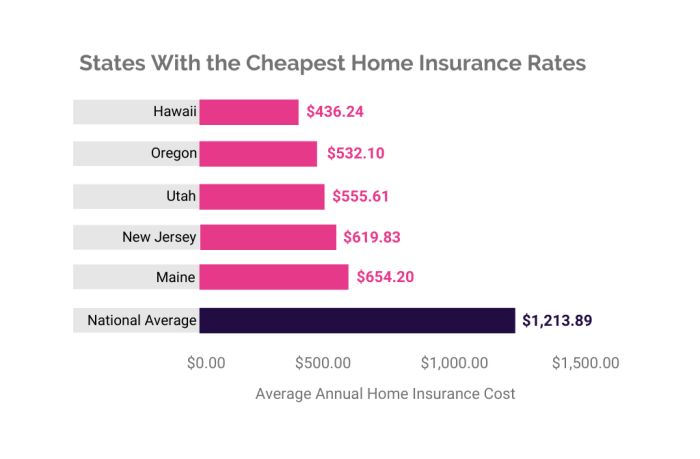

Factors affecting home insurance rates in high-risk areas

Location plays a significant role in determining home insurance rates, especially in high-risk areas. Insurance companies take into account various factors when assessing the risk associated with a particular location, which ultimately influences the premiums that homeowners have to pay.

Impact of Location on Insurance Rates

One of the primary factors that affect home insurance rates in high-risk areas is the location itself. Properties located in areas prone to natural disasters such as floods, earthquakes, hurricanes, or wildfires are considered high-risk by insurance companies. The proximity to bodies of water, fault lines, or dense forests can significantly impact the likelihood of property damage, leading to higher insurance premiums.

Risk of Natural Disasters

The risk of natural disasters is a crucial factor that influences insurance costs in high-risk areas. Homes located in regions prone to frequent natural calamities are more expensive to insure due to the increased probability of damage. Insurance companies factor in the potential risk of hurricanes, earthquakes, tornadoes, or wildfires when determining the premiums for homeowners in these areas.

Other Factors Affecting Insurance Costs

In addition to the risk of natural disasters, other factors such as crime rates in the neighborhood can also impact home insurance rates. Higher crime rates indicate a greater likelihood of theft, vandalism, or property damage, which can lead to increased insurance premiums. Insurance companies consider various risk factors when calculating the cost of home insurance in high-risk areas, including the overall safety and security of the neighborhood.

Strategies to reduce home insurance costs in high-risk areas

When living in a high-risk area, it’s essential to find ways to reduce home insurance costs while still maintaining adequate coverage. By implementing certain strategies, homeowners can potentially lower their premiums and save money in the long run.

Improving home security

Enhancing home security measures can significantly impact insurance rates in high-risk areas. Installing security systems, motion-sensor lights, deadbolts, and smoke detectors can help protect your home against potential risks, making it less susceptible to theft, vandalism, or damage. Insurance companies often offer discounts for homes with improved security features, so investing in these upgrades can lead to cost savings on premiums.

Bundling insurance policies

Another effective strategy to reduce home insurance costs in high-risk areas is to bundle multiple insurance policies with the same provider. By combining home insurance with auto, life, or other insurance policies, homeowners can qualify for discounts and lower overall premiums. Bundling insurance policies not only saves money but also simplifies the insurance process by having all policies under one provider.

Renovations or upgrades, Cheapest home insurance for high-risk areas

Making renovations or upgrades to your home can also help lower insurance rates in high-risk areas. Upgrading the roof, electrical systems, plumbing, or HVAC systems can reduce the likelihood of damage from natural disasters or accidents, ultimately decreasing the risk for insurance providers. Additionally, renovations that enhance the structural integrity of the home, such as storm-resistant windows or reinforced doors, can lead to further discounts on insurance premiums.

Comparison of insurance providers offering coverage in high-risk areas: Cheapest Home Insurance For High-risk Areas

When it comes to finding home insurance in high-risk areas, it’s crucial to compare different insurance providers to ensure you get the best coverage at a competitive rate. Here, we will detail some of the insurance companies specializing in high-risk areas, their coverage options, limitations, and the costs and benefits of their policies.

State Farm Insurance

State Farm Insurance is a well-known provider that offers coverage in high-risk areas. They provide comprehensive coverage for various risks, including natural disasters and theft. However, their premiums can be on the higher side compared to other insurers.

Allstate Insurance

Allstate Insurance is another popular choice for homeowners in high-risk areas. They offer customizable coverage options to tailor the policy to your specific needs. While their premiums may be competitive, some limitations on coverage for certain high-risk areas may apply.

Nationwide Insurance

Nationwide Insurance is known for its flexible coverage options for homeowners in high-risk areas. They provide a range of discounts that can help reduce insurance costs. However, it’s essential to review their policy limitations and exclusions carefully.

Progressive Insurance

Progressive Insurance is a reputable insurer that offers coverage in high-risk areas. They provide innovative solutions and competitive rates for homeowners facing risks such as floods or wildfires. Be sure to compare their policy benefits and limitations with other insurers.

USAA Insurance

USAA Insurance specializes in coverage for military members and their families, including those living in high-risk areas. They offer unique benefits and discounts for policyholders. However, eligibility criteria may apply, so it’s essential to check if you qualify for coverage.

Comparing Costs and Benefits

When comparing insurance providers in high-risk areas, it’s crucial to consider not only the costs but also the benefits and coverage options. Look for insurers that offer comprehensive coverage for the risks you face while providing competitive rates. Additionally, consider any limitations or exclusions in the policies that could impact your coverage in high-risk areas.

Importance of proper coverage despite higher costs

Proper coverage is essential for homeowners in high-risk areas, despite the potentially higher costs. In disaster-prone regions, the risks of being underinsured can be catastrophic, leaving homeowners financially vulnerable in the face of natural disasters or other unforeseen events.

Risks of being underinsured in disaster-prone regions

In disaster-prone regions, such as coastal areas prone to hurricanes or regions susceptible to wildfires, being underinsured can have devastating consequences. Homeowners may find themselves unable to fully rebuild or repair their homes after a disaster, leading to financial strain and potential homelessness. Without adequate coverage, homeowners may be left with significant out-of-pocket expenses, putting their financial stability at risk.

- Underinsurance can result in insufficient funds to cover repairs or reconstruction of the home.

- Homeowners may struggle to replace personal belongings lost in a disaster without proper coverage.

- Inadequate coverage can lead to delays in recovery and prolonged financial hardship for homeowners.

Examples of how proper coverage can protect homeowners financially

Proper coverage in high-risk areas can provide homeowners with peace of mind and financial security in the event of a disaster. Insurance policies that adequately cover the cost of rebuilding or repairing a home can help homeowners recover and rebuild their lives without facing insurmountable financial burdens.

For example, a homeowner in a flood-prone area who has flood insurance can receive compensation for damages to their home and belongings, allowing them to rebuild and recover without bearing the full cost.

- Adequate coverage can help homeowners avoid financial ruin and ensure they can rebuild their lives after a disaster.

- Proper insurance can provide homeowners with the necessary resources to repair or replace damaged property and belongings.

In conclusion, prioritizing proper coverage is key when residing in high-risk areas. By understanding the nuances of insurance rates and providers, homeowners can make informed decisions to safeguard their investments effectively.

When choosing a home insurance policy, it’s important to consider adding riders and endorsements for extra protection. These additions can provide coverage for specific items or situations that may not be included in a standard policy. Learn more about home insurance policy riders and endorsements to ensure you have comprehensive coverage for your property.

Protecting your personal belongings is a crucial part of homeowners insurance. In the event of theft, damage, or loss, having the right coverage can make all the difference. Find out how to safeguard your possessions with the right policy by exploring homeowners insurance for personal belongings.

Understanding the difference between flood insurance and homeowners insurance is essential for homeowners in at-risk areas. While homeowners insurance may cover some water-related damages, it typically does not include floods. Discover the benefits of having separate flood insurance and how it compares to homeowners insurance by reading more about flood insurance vs. homeowners insurance.

{kind=link}